I paid off $33,850 of student loan debt in just over four years. Here’s Part 2 of how I did it.

My first step in paying off my student loans was to spend $500 a month paying off one high interest student loan that I transferred to a 0% APR credit card. This was in addition to paying $300 a month to meet the minimums on my other student loan payments.

The next step to paying off my student loans was a controversial one: make only minimum payments for years.

Make Minimum Payments and Invest at Higher Returns

I became somewhat infamous in the personal finance world with one of my first blog posts entitled Don’t Pay Off Your Student Loans. In this article I explained how it is possible to make extra money if you can invest money at a higher interest rate than you pay on your debt.

It was true then and it’s true today.

If the interest rate on your student loans is less than 3% (which mine were, thanks to variable interest rates and the Federal Reserve), all you need to do is find an investment that gets more than a 3% return and you’re better off investing than paying off the loans.

The stock market is one way to try to get big returns on your investments, but it is very risky and you can lose a lot of money there. I used to do a lot of active investing and trading, but I found that I was doing a lot of work and wasn’t making any money.

I still have a lot of money in the stock market between my Roth IRA and 401k, but my rate of return has been pretty crappy ever since I made 28% back in 2010.

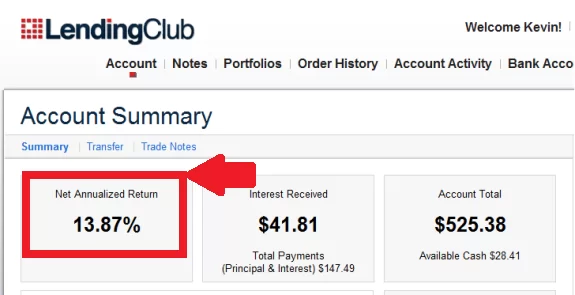

I’ve found I can get better and safer returns with peer to peer lending, such as LendingClub.com. As you can see, I’m getting returns better than 13% in my Lending Club account, which is more than 10% greater than my student loans.

A lot of people (including most personal finance bloggers) ignore the math behind this reality and claim that all debt is bad debt. They are wrong.

If you are confident in your ability to invest your money at a higher rate of return then you are paying on your debt, mathematically it makes perfect sense to do so.

The problem is that investment returns are never guaranteed, while paying off debt is essentially a guaranteed return. It is also much easier to pay down debt than it is to successfully invest money.

Finally, there is a mental aspect of being debt free that each person must consider. If the idea of owing someone money makes you lose sleep at night, then a higher rate of return isn’t worth it.

If I Could Do it All Over Again…

I spent about two years making only minimum payments and investing what I would have used to pay off debt. And if I could do it all over again, I would have done things a little differently.

- I would have had a more balanced approach of paying down debt as well as investing, instead of investing everything over the minimum payments

- I would have put more in Lending Club and less in the stock market

- For my stock market investments, I would have invested more in index funds and less in call options

Overall I tried investing aggressively and I probably would have been better off paying down debt. This brings me to the third and final step of paying off my student loans, which I’ll discuss tomorrow.

Readers: How do you feel about debt? Would you rather pay off low interest debt, or make minimum payments and try to invest for a greater return?

Kevin McKee is an entrepreneur, IT guru, and personal finance leader. In addition to his writing, Kevin is the head of IT at Buildingstars, Co-Founder of Padmission, and organizer of Laravel STL. He is also the creator of www.contributetoopensource.com. When he’s not working, Kevin enjoys podcasting about movies and spending time with his wife and four children.

I totally agree with this approach. It’s essentially an arbitrage opportunity where you’ve borrowed at a lower rate and can lend at a higher rate. Nothing wrong with that.

My only issue is I hate the tax situation that Lending Club and Prosper creates where you have to itemize every single loan. It gets even more hairy if you have any charge-offs.

I would do it if the loans were fixed rate. I figure rates will have to go up sometime in the next couple years and I wouldn’t want to get stuck with a variable loan at that point. However, withmy mortgage I expect CD rates to exceed my mortgage rate sometime in the next 10 years so I don’t know that I will be paying that off very fast. Time will tell.

I pay the minimum payment on my SL (since the rate is so low) and use my free capital to invest and in the near future to pay for day care (damn is it ever expensive).

If/When the rate on my student loans goes up, I’ll just pay them off faster.

I see your reasoning behind investing and paying minimum payments. I think the best thing is to have a balance between the two like you said. Right now we are leaning more towards the paying down debt because it provides us with piece of mind. After our debt is gone other than our mortgage we will get more into investing (and possibly lending).

less in call-options? Really? Didn’t know you were using options…

Could you do a post on your experience with and options on options at some point?

I agree with you in theory but I HATE debt and want to be done with it forever, or at least until I decide I want to buy a house.

Can you write a post about your experience with Lending Club? I’m debt-free and interested in potentially using the Lending Club as an investment vehicle, but would like to hear your thoughts.

Ditto!

My coworker and I have discussed investing in Lending Club with our “play money” and was interested with your experience with them and if you ever compared Prosper and Lending Club.

Looks like there is a lot of interest in this topic.

I’ll do a post next week about my experiences with Lending Club. Overall it’s been good so far since I have more money today than I did when I started. 🙂

Another point to add to this idea is that on a loan you’re usually paying interest based on a ‘daily rate’ so over time, as your loan shrinks, you’re paying less and less interest. But if you invest in dividend paying stocks, you’re dividends can be used to buy more stock, and more and more – you’re compounding interest. As long as the company keeps paying dividends, you should be coming out ahead (assuming similar dividend and interest rates).

i had to admire your great effort, you have shared valuable information with us thanks for the good workhttp://www.cinemacuritiba.com